On paper, sourcing value alternatives for finishes sounds straightforward. You take a specified product, look for something equivalent, compare prices, and move on. In reality, anyone who has tried to do this properly knows it is anything but simple.

The finishes market is vast, fragmented, and unevenly documented. For any given tile, carpet, sanitaryware item, or wall finish, there are dozens – sometimes hundreds – of possible alternatives in the market. Many of them are viable. Many are not. The challenge is not the lack of options, but the effort required to identify the right ones.

A useful way to think about this is to compare it to search. If you were looking for information online, you would not be satisfied if your search engine only scanned three or four websites before giving you an answer. You would expect it to look across the entire web, filter out what is irrelevant, and surface the most useful results. Anything less would feel incomplete.

Yet this is effectively what happens when value alternatives are sourced manually.

Most manual sourcing starts with what is familiar. Known suppliers. Previous projects. A small circle of trusted contacts. This is understandable. When time is limited, people work with what they know. But it also means the search is inherently constrained. It reflects personal reach rather than the full depth of the market.

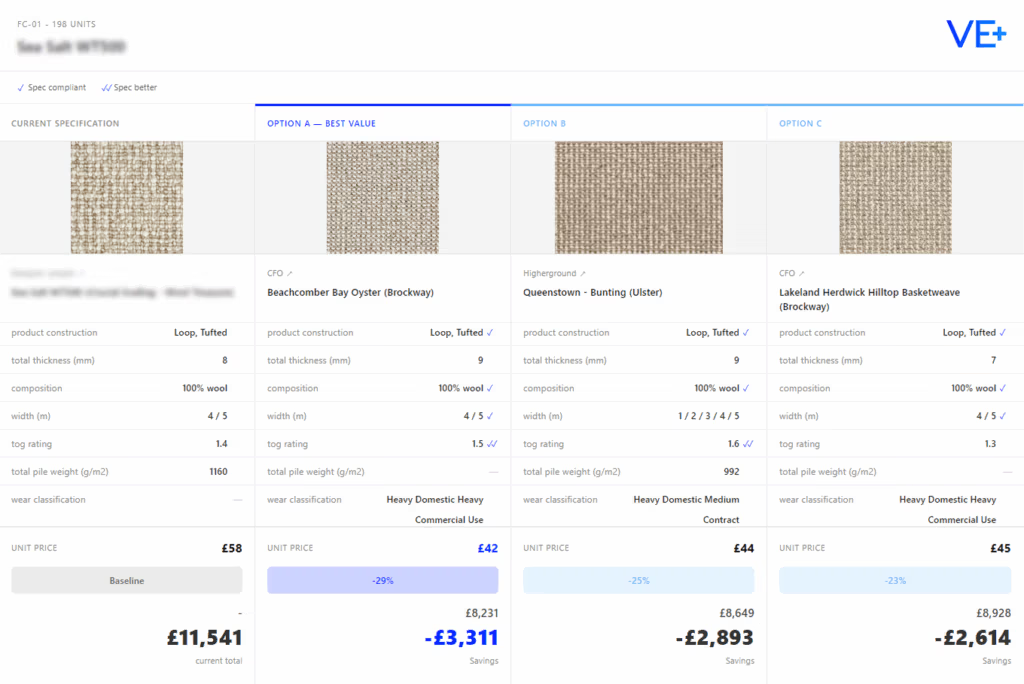

To properly assess value alternatives, the market needs to be scanned in depth. That means engaging with a large number of suppliers, reviewing technical and commercial information, and filtering options against the original specification. It is a systematic process, not a quick comparison, and it requires broad coverage to be meaningful.

In practice, this work is still done through emails, PDFs, spreadsheets, and follow-ups. Information arrives in different formats, at different speeds, and with varying levels of detail. Comparing like-for-like becomes slow and manual, especially when teams are working under live tender or procurement deadlines.

The result is that manual sourcing tends to fall short. Either the search remains shallow, missing better value options that sit outside familiar networks, or it becomes so time-consuming that it cannot realistically be repeated across multiple packages and projects. In both cases, decisions are made with partial visibility of the market.

This is not a failure of people or intent. QSs and pre-con teams understand the importance of value alternatives. The limitation is structural. The finishes market was never designed to be scanned manually at scale, particularly within the timeframes modern projects demand.

At VE+, we started from this exact frustration. We believe that if value alternatives are to be taken seriously, the way the finishes market is explored has to change. Not by asking teams to work harder, but by enabling deeper, broader market scanning without adding time pressure.