On high-end residential and hospitality projects, the lighting package is rarely reopened once specified. It sits in the cost plan, often running well into six figures, while procurement teams work through other line items around it. The prevailing assumption is that it is too complex to benchmark and too closely tied to the design intent to be separated from the original specification.

That assumption is not entirely wrong. The comparison genuinely spans shape, finish, materiality, beam angle, colour temperature, output levels, dimming protocol, certification requirements, and supplier credibility, often simultaneously, across twenty or more line items. Unlike a structural material or a finishing product, where equivalence is relatively observable, lighting sits at the intersection of technical performance and aesthetic intent. The perceived risk of disturbing the scheme makes the category feel protected.

But structural complexity is not the same as price opacity. Much of the spread between products at a similar specification tier reflects something quite different: brand positioning, distribution margin, and the narrowness of the market that most procurement teams can see at the moment of benchmarking.

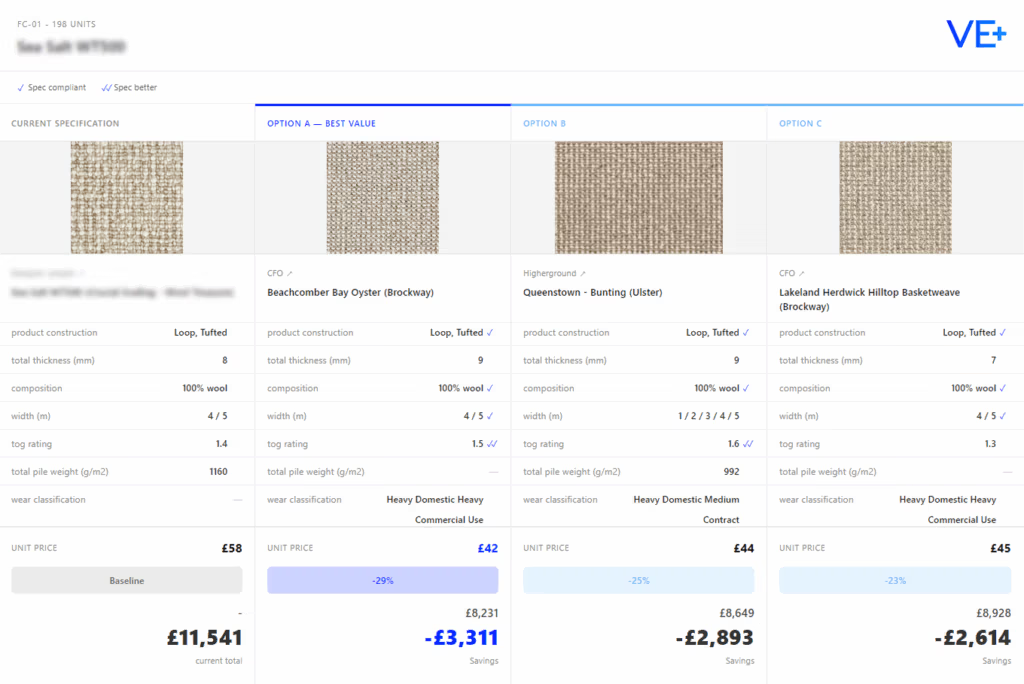

Price spreads of 50–60% between products with near-identical specification and comparable design intent are observed frequently in this category. This is not a consequence of performance difference. It is a consequence of market structure – a relatively small number of well-known brands command premium positions that are rarely challenged because the broader supply landscape is not easily visible at the pre-construction stage. The complexity of comparison is real, but it functions as an institutional reason not to look further.

A recent single-line item illustrates the pattern. A project running 68 units of one fitting was benchmarked against a like-for-like alternative. The match was identified and approved quickly, generating a saving of over £25,000 on that specification alone. The result was not exceptional; it reflected a normal price spread in a category where the specified product carried a margin that the market simply does not require.

Scaled across a full lighting package of fifteen to twenty line items, the cumulative opportunity is typically substantial. The package does not need to be redesigned. The design intent does not need to shift. What changes is the range of the market being considered at the tender stage.

Lighting is an unusual category in this respect. The gap between what is visible to procurement teams and what the market actually offers is persistently wide. Unlike other materials categories where price comparison is increasingly routine, lighting continues to be treated as a specialist area where brand familiarity substitutes for benchmarking, often without the assumption being examined.

At VE+, this is a category we approach with particular attention, not because the comparison is straightforward, but because the distance between assumed complexity and available market is wider here than in almost any other specification category.